A senior manager gets a clean performance review in January. Good feedback, strong year, no reason to expect anything different. By March, the role is gone. Restructuring. The mortgage payment didn't change. The private school tuition didn't change. The car payment, the 529 contribution, the insurance premiums: all of it kept running, on schedule, as if nothing had happened.

That's the structure working exactly as designed. The problem is what it was designed around.

Most financial plans for high earners are built on a single assumption so obvious it rarely gets stated: the income continues. The mortgage was sized to it. The savings rate was calibrated to it. The fixed commitments, one by one, were each reasonable given the paycheck. Nobody modeled what happens when the paycheck stops.

This isn't a structural flaw, exactly. It's an untested one. The same habits that build a strong financial position, committing early, automating, maximizing contributions, taking on a mortgage that stretches a little, are the habits that make the structure fragile when income disappears. Every dollar locked into a fixed obligation is a dollar that can't adjust.

High earners face a specific version of this problem. The commitments scale with income. The lifestyle, the housing, the education choices: all of them reflect what the income can support, not what a household can sustain without it. Most people haven't calculated the gap between those two numbers.

Three Places the Gap Shows Up First

When income stops, the exposure surfaces in three areas, usually in this order.

Cash flow coverage is the first problem. Fixed obligations don't pause. Mortgage, car, insurance, debt service: these run regardless of what's happening with employment. The question is how long liquid assets can cover them without touching retirement accounts or selling investments at the wrong time. Most people haven't done that calculation. They know they have savings. They don't know how many months those savings represent against their actual fixed cost structure.

Benefits continuity is the second. Employer-sponsored health insurance ends, typically at the end of the month of separation or the end of the following month depending on plan terms. COBRA extends coverage but at full cost, often $1,500 to $2,500 per month for a family. That's a new fixed cost that wasn't in the original budget. According to the U.S. Department of Labor, qualified individuals can be required to pay the full cost of coverage plus a 2% administrative fee. Disability insurance, if it exists at all, usually comes from the employer too. It disappears with the job. The moment a household most needs protection is often the moment the protection lapses.

Liquidity runway is the third. An emergency fund that covers three to six months of expenses looks different when "expenses" means a $4,500 mortgage, $3,200 in childcare, and $800 in insurance premiums in addition to everything else. The standard rule of thumb was calibrated to average household costs. High earners with significant fixed obligations need a longer runway, and often have the same three-to-six-month buffer they built years ago, before the commitments grew.

What Stress-Testing Actually Looks Like

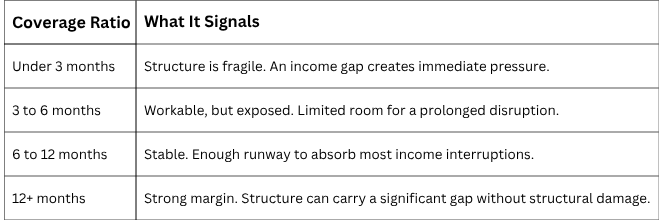

This is a single calculation, not a forecast. Pull up the fixed monthly obligations: mortgage, debt service, insurance, tuition, everything on autopay. Add them up. Divide your liquid savings by that number. The result is your fixed cost coverage ratio, expressed in months.

Here is what that number means in practice:

Most high-income households assume they're in the second or third category. Many are not, because the buffer was sized years ago and the fixed obligations grew around it.

Then ask two questions. First, which of those obligations could actually be paused or renegotiated in a disruption, and which couldn't? Second, if the number is low, what's the most practical way to close the gap while still employed?

The options are limited and familiar: increase liquid reserves, reduce or refinance fixed obligations, establish a HELOC while income is intact, or separate key insurance coverage from employment. None require drastic changes. But knowing the number is the prerequisite for any of them.

That distinction matters more now than it did a few years ago. Job security in professional roles has become less predictable. Restructurings happen to strong performers. The performance review and the layoff notice can share the same quarter. A financial structure that was never tested against that scenario isn't wrong. It's just incomplete.

If you want to think through how disability coverage and emergency fund sizing fit into this picture, Quiet Protection for Busy Families and Building an Emergency Fund When Life Feels Full cover both in more detail. And if you've recently been through a layoff announcement, even as a survivor, Your Company Just Announced Layoffs. You Still Have Your Job. addresses what that moment tends to surface financially.

Frequently Asked Questions

How long does COBRA coverage last, and what does it typically cost?

COBRA allows you to continue your employer-sponsored health insurance for up to 18 months after separation. The cost is the full premium, both the portion you paid and the portion your employer covered, plus a 2% administrative fee. For a family plan, that often runs between $1,500 and $2,500 per month. It's real coverage, but the cost is a significant addition to a household budget that's already under pressure from lost income.If I have disability insurance through my employer, am I covered if I lose my job?

Employer-provided disability insurance generally ends when employment ends. It covers disability while you're employed, not after separation. If income disruption from job loss is the concern, disability insurance doesn't address it. That's where emergency fund runway and, in some cases, individual disability policies become relevant. Individual policies stay with you regardless of employer.How much should an emergency fund cover for a high-income household?

The common guidance, three to six months of expenses, was built around average household budgets. For households with significant fixed obligations, the relevant number is how many months of those specific fixed costs your liquid savings can cover. That calculation is more useful than a percentage of income. Many households find their buffer covers less time than they assumed once fixed costs are itemized.What's a fixed cost coverage ratio, and how do I calculate mine?

It's your total liquid savings divided by your monthly fixed obligations. If you have $60,000 in liquid savings and $10,000 in monthly fixed costs, your coverage ratio is six months. The ratio tells you how long your structure can run without income before you'd need to draw on retirement accounts, sell investments, or make structural changes. Calculating it once tends to clarify the picture quickly.Does this mean I should reduce my fixed commitments?

Not necessarily. The point isn't that fixed commitments are mistakes. It's that most households never calculate the margin between their structure and an income gap. In some cases the margin is adequate. In others, a targeted adjustment, a larger liquid reserve, an individual disability policy, a HELOC established while employed, closes the gap without requiring lifestyle changes. The first step is knowing the number.Ready to see how planning can support your goals? It starts with a conversation.

D'Agaro Financial Advisory is a Registered Investment Adviser located in Virginia. Registration does not imply a certain level of skill or training. This content is for educational purposes only and is not tax, legal, or investment advice.